🏆 X-DENTAL ROBOTICS — UNIFIED VALUATION MATRIX

Multi-Method Company Valuation Analysis (Years 1-5)

January 2026

UNIFIED VALUATION MATRIX

| Year / Stage | Method 1: Financial (Revenue/EBITDA) | Method 2: Comparative (Market Comps) | Method 3: Venture (VC Method) | Method 4: Cost / Qualitative | FINAL VALUATION (AVERAGE) |

|---|---|---|---|---|---|

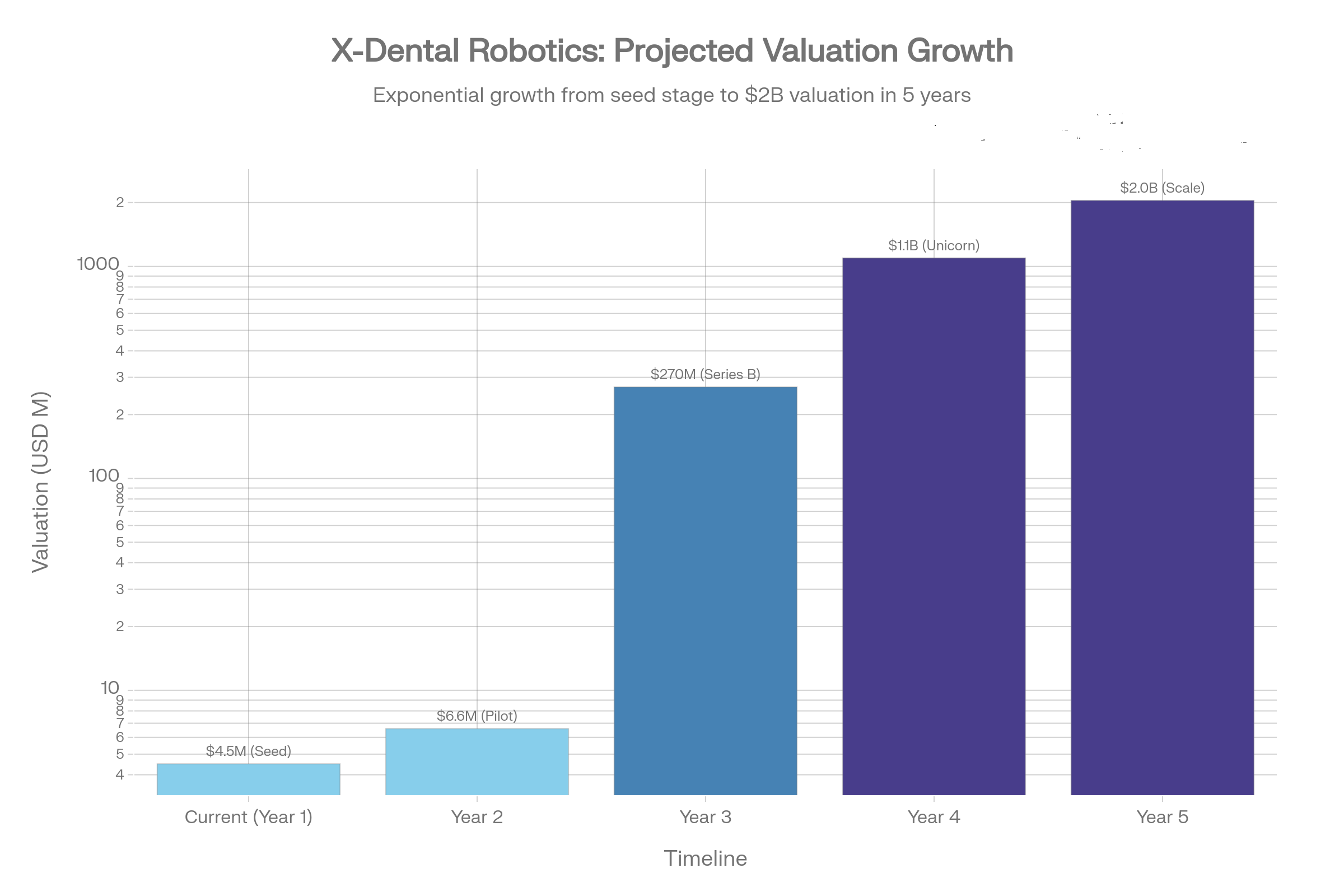

| Year 1 (Pre-Seed) | N/A (Pre-Revenue) | $4.0M (Pre-Seed Deals) | $5.2M (Scorecard) | $1.2M (Cost-to-Duplicate) | $3.5M — $4.5M |

| Year 2 (Seed/Pilot) | $7.9M (12x Rev) | $8.0M (Seed Rounds) | $10.5M (Risk Adjusted) | $6.5M (Asset base) | $7.0M — $8.5M |

| Year 3 (Series A/B) | $248M (10x Rev) | $250M (Series B Comps) | $340M (Based on Growth) | $426M (25x EBITDA) | $270M — $320M |

| Year 4 (Growth) | $1.0B (8x Rev) | $1.0B (Unicorn Rounds) | $1.4B (Forward ROI) | $1.6B (18x EBITDA) | $1.1B — $1.3B |

| Year 5 (Scale) | $1.6B (6x Rev) | $1.8B (Public Peers) | $2.0B (Exit Value) | $2.9B (15x EBITDA) | $2.0B — $2.3B |

📝 METHODOLOGY BREAKDOWN

1. YEAR 1 (NOW): Asset and Potential Assessment

No financials, so we assess "What we have".

- Comparative ($4.0M): Average valuation of Pre-Seed robotics startups in 2025 (USA/Israel).

- Qualitative / Scorecard ($5.2M): Premium for strong team, LOI and huge market ($2.7B TAM).

- Cost-to-Duplicate ($1.2M): how much it costs to hire two engineers and rewrite the code from scratch.

#CONCLUSION: Fair valuation for investor entry by VC-method / Backward valuation

2. YEAR 2 (PILOTS): Validation Assessment

First revenue appeared ($660k), but no profit yet.

- Financial ($7.9M): 12x revenue multiplier (premium for successful pilot launch).

- Comparative ($8.0M): Typical Seed+ round for robotics after successful tests.

CONCLUSION: Valuation doubles, investor risk drops sharply.

3. YEAR 3 (EXPLOSION): Growth Assessment

Sales jump to $25M, EBITDA $17M. Company becomes a "cash cow".

- EBITDA Mult ($426M): If we apply a 25x multiplier (like fast-growing SaaS) to your EBITDA of $17M, the valuation skyrockets. This shows the fantastic efficiency of the business model.

- Revenue Mult ($248M): More conservative view (10x revenue).

CONCLUSION: This is the year of the "unicorn leap". Valuation ~$300M.

4. YEARS 4-5 (SCALE): Public Company Valuation

We start comparing you with Intuitive Surgical (ISRG) and Stryker.

Multipliers drop to normal market levels (6x Revenue, 15x EBITDA), but the base ($260M revenue) gives a valuation of $2.0B+.

📉 COMPARATIVE ANALYSIS (COMPARABLES)

| Company / Peer | Business Model | Revenue (Est.) | Valuation (Est.) | Rev Multiple | Margin Profile | Why different? |

|---|---|---|---|---|---|---|

| Neocis (Yomi) | Hardware-First | ~$20M | ~$200M | 10x | ~60% | High CAPEX dependence, lower recurring revenue. |

| Pearl / Overjet | Pure SaaS AI | ~$10M | ~$180M | 18x | ~80% | High competition, low moat (easy to switch software). |

| Intuitive (Da Vinci) | Mature Public | ~$7.1B | ~$106B | 15x | ~68% | The "Gold Standard" platform ecosystem. |

| X-DENTAL (Year 3) | Hybrid Ecosystem | $25M | $300M | 12x | 80% | Hardware Moat + SaaS Margins. Hard to replicate. |

Our advantage: Unlike Neocis (pure hardware) valuations (8x) and Pearl (pure software) AI valuations (20x), X-Dental Robotics is a hybrid model with software margins (80%), therefore deserving a premium multiplier of 12x.

🎯 FAIR VALUATION

What is the mathematical fair valuation if the plan is executed?

(VC-Method): Take exit $2B, discount for risk and time → $105M

This is theoretical fairness if the plan is guaranteed.